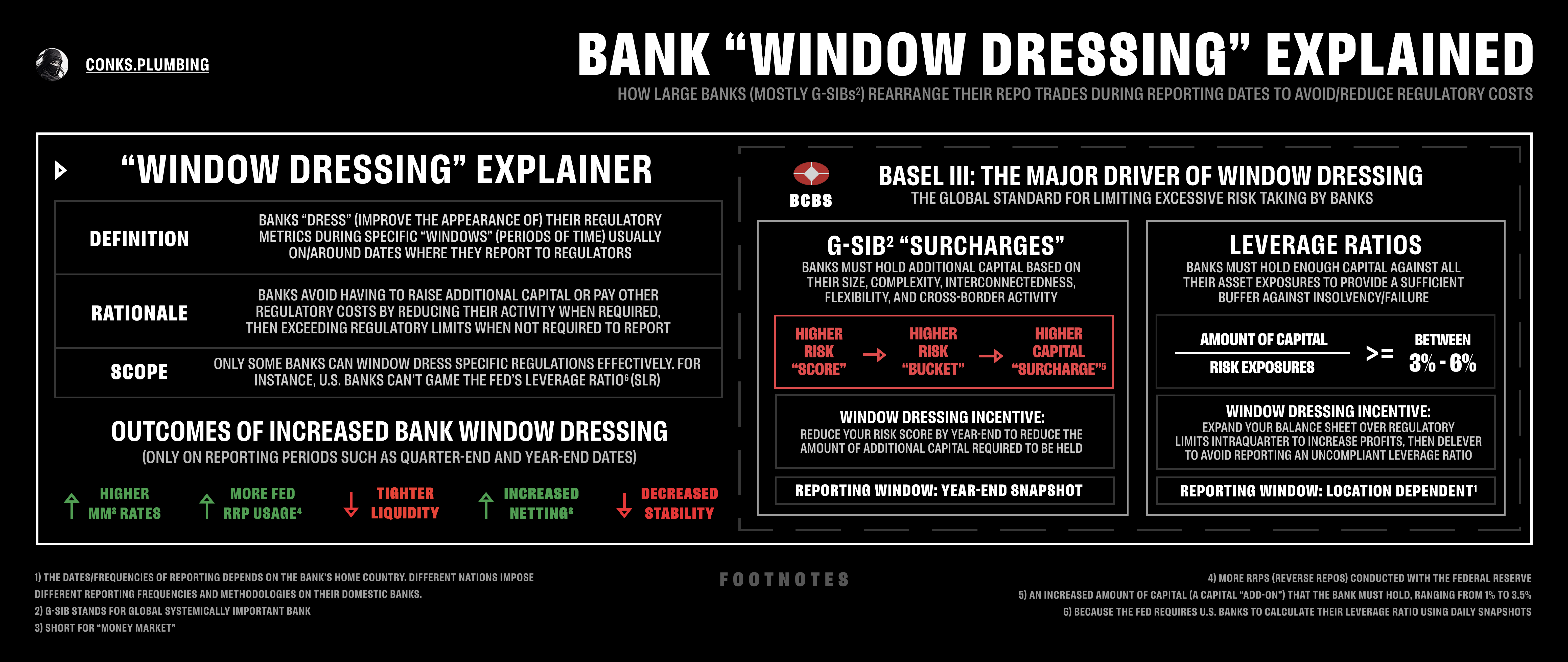

A longstanding loophole exploited by banks globally is set to evaporate. By preventing the most notorious instances of “window-dressing,” a frowned-upon practice designed to skirt regulatory constraints, the global regulatory complex will soon deter banks from evading rules imposed on them following the Great Financial Crisis (GFC). Subsequently, the signature “rate spikes” emerging in repo markets on key financial dates may not only become less extreme but more infrequent. Monetary leaders’ attempt at a “great flattening” has been initiated.

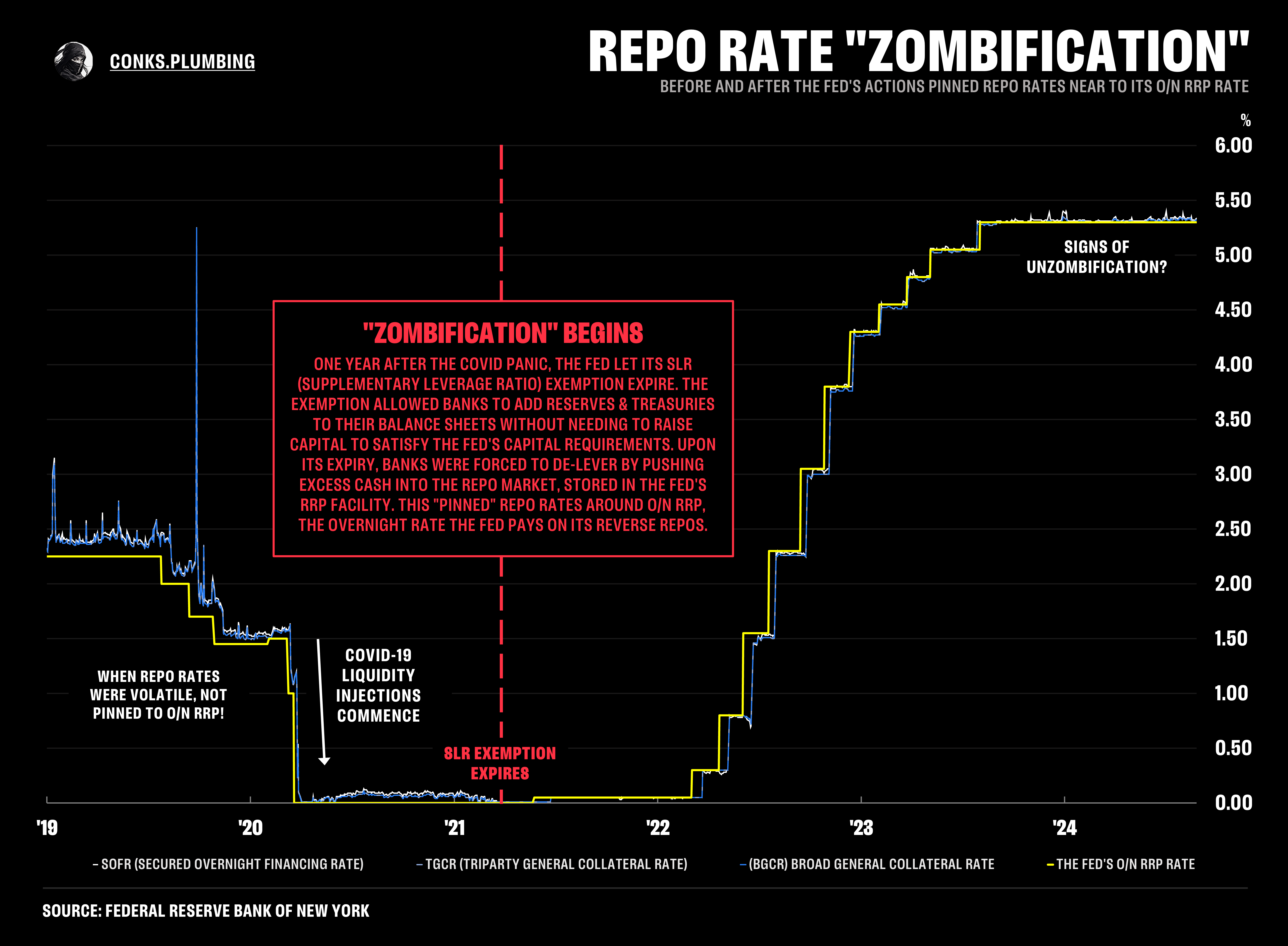

At the end of December 2023, the Federal Reserve’s RRP (reverse repo) facility — the U.S. central bank’s “shock absorber” for excess dollars unable to be invested elsewhere — continued to drain. Plunging toward zero, the Fed’s facility had shed trillions in surplus cash now fleeing to higher-yielding assets such as t-bills, flows that would soon alter the dynamics in repo markets. The enormous overload of money that had poured into repo markets via the Fed’s COVID-19 liquidity injections was about to dry up, prompting market participants to begin to trade primarily among themselves. Instead of rates remaining pinned to the overnight rate the Fed paid on its RRPs — dubbed O/N1 RRP, private sector entities would start to determine where most repo rates printed. The total “unzombification” of repo markets was fast approaching.

Suddenly, however, on December 29th, 2023, the multi-trillion-dollar descent in the level of Fed RRPs was halted temporarily by a ~$200 billion rise in volume. Repo rates simultaneously began to skyrocket, with the cost to borrow cash in the interdealer (GCF) and dealer-to-customer (DVP) markets — ultimately financing the elaborate trades of hedge funds and others — rising sharply. The cause? Yet another “quarter-end”: the last day of each quarter on the financial calendar and the most likely to encounter volatility. As with most quarter-end (but especially year-end2) dates, the prominent repo dealers were pulling back severely from market-making in the most crucial dollar funding ecosystem. The trading desks of the major broker-dealers and dealer subsidiaries of the largest banks (BHCs) — all operating as primary dealers — delayed their duties to unwind or rearrange trades linked to the most infamous regulatory exploit in the modern era.

{kind=link}

For a decade or so, via one method or another, the banking giants have bypassed numerous constraints proposed by the Basel III Accords, a sea of regulations introduced after the GFC to limit excessive bank risk-taking “once and for all.” In what’s known as “window-dressing,” some dealers (primarily foreign dealers) have yet to be required to declare their regulatory metrics using daily averages, the absence of which has allowed them to expand their balance sheets over lengthy periods in which they don’t need to reveal costly or uncompliant exposures to regulators. Before the deadline to disclose their activities, banks have quickly unwound their soon-to-be illicit trades.

Rather than serving as fully active market makers on “period-end” dates, such as quarter-ends and year-ends, dealers have been rewiring their balance sheets to appear as if they took much less risk during certain timeframes than in practice. Consequently, on and around crucial reporting periods, banks’ window-dressing has created temporary “air pockets” of illiquidity (even turmoil) in repo markets. Because most repos3 — short-term cash loans secured against collateral — can be rolled over forever but unwound swiftly the next day, these are the first assets to be dumped by banks whenever they hold excess exposures and reporting dates grow near. Liquidity in repo markets thus grows scarce. Rates must adjust higher to attract those willing to make markets with limited balance sheets, ultimately provoking infamous rate spikes.

At the end of December 2023, the largest repo liquidity providers were either reducing or reshuffling their balance sheets to report more favorable metrics, inducing one of the most bizarre yet typical scenarios in money markets. With regulatory limits now compulsory, banks with available but inflexible balance sheets stepped in by lending cash to dealers and other market participants at hefty spreads. Rates even surpassed what the Fed offered via its Standing Repo Facility (SRF), a mechanism that supposedly enforced an upper limit on repo rates. Since the SRF was set to open (as usual) at 1:30pm — long after the peak repo trading hours of 8-10am, dealers were forced to secure dollars via private markets at rates above the Fed’s repo “ceiling.” Meanwhile, with their usual dealer counterparties unwilling to provide liquidity, money market funds (MMFs) — the major cash investors in repo markets — were forced to accept a lower return on their cash by parking it at the Fed’s RRP facility.

Although somewhat defective, the Fed’s tools for enforcing upper and lower limits in its repo hierarchy were able to stem a full-blown liquidity squeeze in both directions — the RRP providing a (soft) rates floor and the SRF providing a (soft) rates ceiling.

Fast forward to today, and repo market participants have witnessed countless further rate spikes on key financial dates. Only last month, SOFR (the Secured Overnight Financing Rate), the Fed’s primary measure of repo rates, rose again to recent heights, causing a stir in the media. With increased money market unrest, regulators appear to have witnessed enough to want to finally avert most, if not all, banks from evading Basel III and provoking market disruptions. The global regulatory complex, following the usual lengthy pause, has reached its near-maximum tolerance for allowing the most observable regulatory arbitrage in dollar funding markets to continue unabated. Officials have commenced a slow purge of the most significant incentives, attempting a Great Flattening of repo rate volatility. Yet, this flattener may prove more difficult than they expect. Catalysts other than the Basel III Accords will continue to spur instability. Let’s dive deeper into the plumbing.