The Fed's Relief Valve: Part I

how officials plan to boost Treasury market liquidity

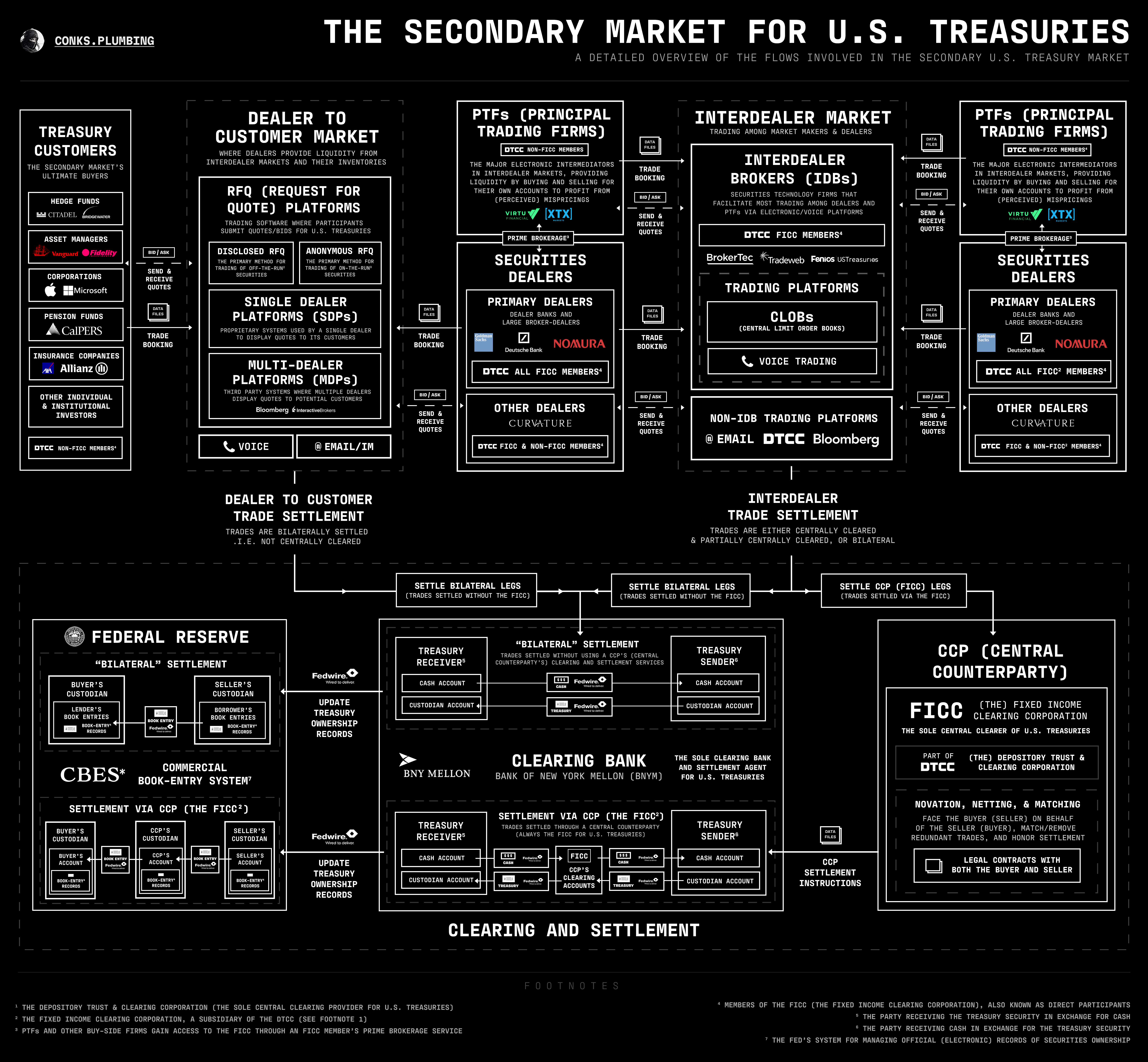

The U.S. Treasury market’s plumbing is about to receive another greasing. In an attempt to boost liquidity and suppress volatility, the latest band of monetary leaders has vowed to lubricate the pipes of America’s sovereign debt market. An enormous debt load and elevated deficits have prompted U.S. central bank and Treasury officials to grow wary of market dysfunction. Treasury Sec. Bessent and POTUS have publicly targeted a lower 10-year yield1 while delaying an increase in longer-term Treasury issuance, sovereign debt that carries increased duration risk2. Leaders at the Fed, meanwhile, have performed a “regulatory 180”, declaring their intention to reduce major constraints on dominant UST (i.e. U.S. Treasury) market makers3. The Fed’s “relief valve” could thus finally be re-opened.

Ever since the GFC (Great Financial Crisis) concluded, the global regulatory complex has imposed increasingly fierce shackles on the major banking giants — all large bank holding companies (BHCs) that operate vast primary dealer businesses. Basel III and The Dodd-Frank Act have transformed these huge “dealer banks”4 from risk-takers into boring utilities, hampered by relentless capital (and liquidity) requirements. To prevent a replay of the GFC, regulators have forced big banks to hold enough capital to offset both the riskiness and size of their balance sheets. Bank risk-taking has been capped by Basel III’s RWA (risk-weighted assets) standard, which mandates banks to maintain “capital buffers”5 above and beyond the riskiness of their exposures. Even so, some “riskless” assets have always turned hazardous eventually6, prompting monetary architects to invent the SLR: the supplementary leverage ratio. Alongside risk-based ratios7, the SLR acts as a “non-risk weighted” constraint, forcing banks to raise equity whenever they expand their balance sheets, no matter the exposure8. With even U.S. Treasuries and bank reserves now labelled as dangerous, the SLR9 has compelled dealer banks to somewhat pull back from providing liquidity in the most systemic regions of global finance.

But with a new POTUS in power, a deregulatory wind is blowing. A series of out-of-the-blue statements by top central bankers suggests the Fed will exempt (i.e. remove) USTs and other exposures from the SLR. Obscure markets that capture constraints on key Treasury market makers10 have thus started pricing in an unwind of the harshest plumbing climate on record, deepened by a vast supply of Treasuries and heightened deficits11. Nevertheless, for numerous political and plumbing reasons, the Fed may fail to deliver a great easing of dealer constraints, an outcome being priced out of — not into — markets. A regulatory “rug pull’ is looming.