The Fed's Plumbing Dilemma

a speculative rush into risk assets may prompt some "plumbing QE"

After neutralizing trillions of dollars in excess liquidity, the Federal Reserve’s “shock absorber” has begun to decompress. Some of the $2 trillion stored in the Fed’s reverse repo facility (the RRP) is attempting to re-enter the banking system. This will not only prevent liquidity from falling to unstable levels but further threaten the U.S. central bank’s tightening stance. The Fed’s “Plumbing Dilemma” is looming.

As Conks anticipated last month, the U.S. central bank’s inaction and silence around its longstanding hawkish stance has caused equities to soar further, while bond yields and the U.S. dollar have, unexpectedly to most, continued to rebound. Yet again, the market has slowly started to realize the Fed’s task of dampening animal spirits will be harder than expected. One of likely many “Transitory Pauses” is now in full effect, with any emergence of recession talk marking another lower bottom in risk assets.

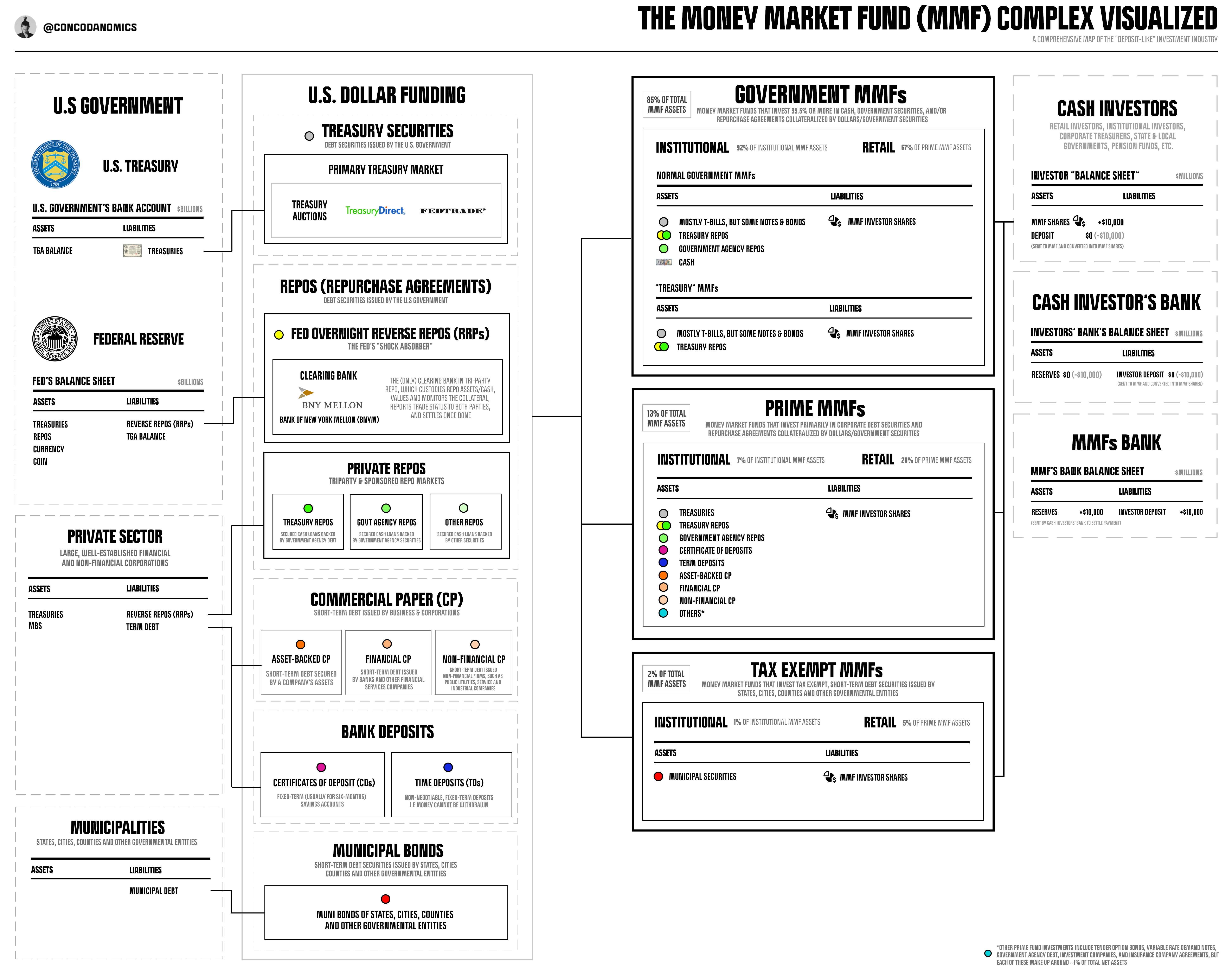

Once again, the Fed’s commitment to subdue animal spirits is about to be tested. Not only have risk assets rallied, housing starts and prices reaccelerated, and labor market conditions remained tight, but now a large pool of excess cash has started to be drawn down by investors. Those seeking even higher yields than an alluring ~5% risk-free return have begun to pull money from money market funds (MMFs), the most cash-like investment vehicle after bank deposits. A speculative spree could be emerging.

Meanwhile, the much-hyped refilling of the U.S. government’s bank account — the Treasury General Account (TGA) at the Fed — has passed its most perilous phase, with only $110 billion shy of the U.S. Treasury’s end-of-September target of $600 billion and liquidity remaining ample.

Trapped liquidity has been pulled from the Fed’s “shock absorber”, the RRP facility, to finance the U.S. government’s ever-increasing spending bill, while also managing to dampen the allegedly sinister effects of the “TGA refill”. Funding the U.S. empire combined with the start of a speculative investor spree has, for the first time since May 2022, caused RRPs conducted by the Fed to drop below $2 trillion outstanding. Ultimately, the monetary plumbing has remained well-oiled throughout a period of heightened fear and uncertainty.

{kind=link}

Money market funds financing the U.S. government by cashing out of RRPs to buy Treasuries is liquidity neutral. Trapped liquidity moves straight from the Fed’s RRP facility into the U.S. government’s bank account, leaving reserves and deposits undisturbed. In contrast, all that’s needed for an RRP drawdown to be stimulative is if investors redeem their MMF shares, obtain bank deposits, and wander down the risk curve. The global pools of money will have travelled from cash-like safe havens to more speculative waters.

{kind=link}

Arriving safely, however, is another question. As history shows, it will be anything but smooth sailing.