— links to part one and part two of the Demystifying the Repo Market series

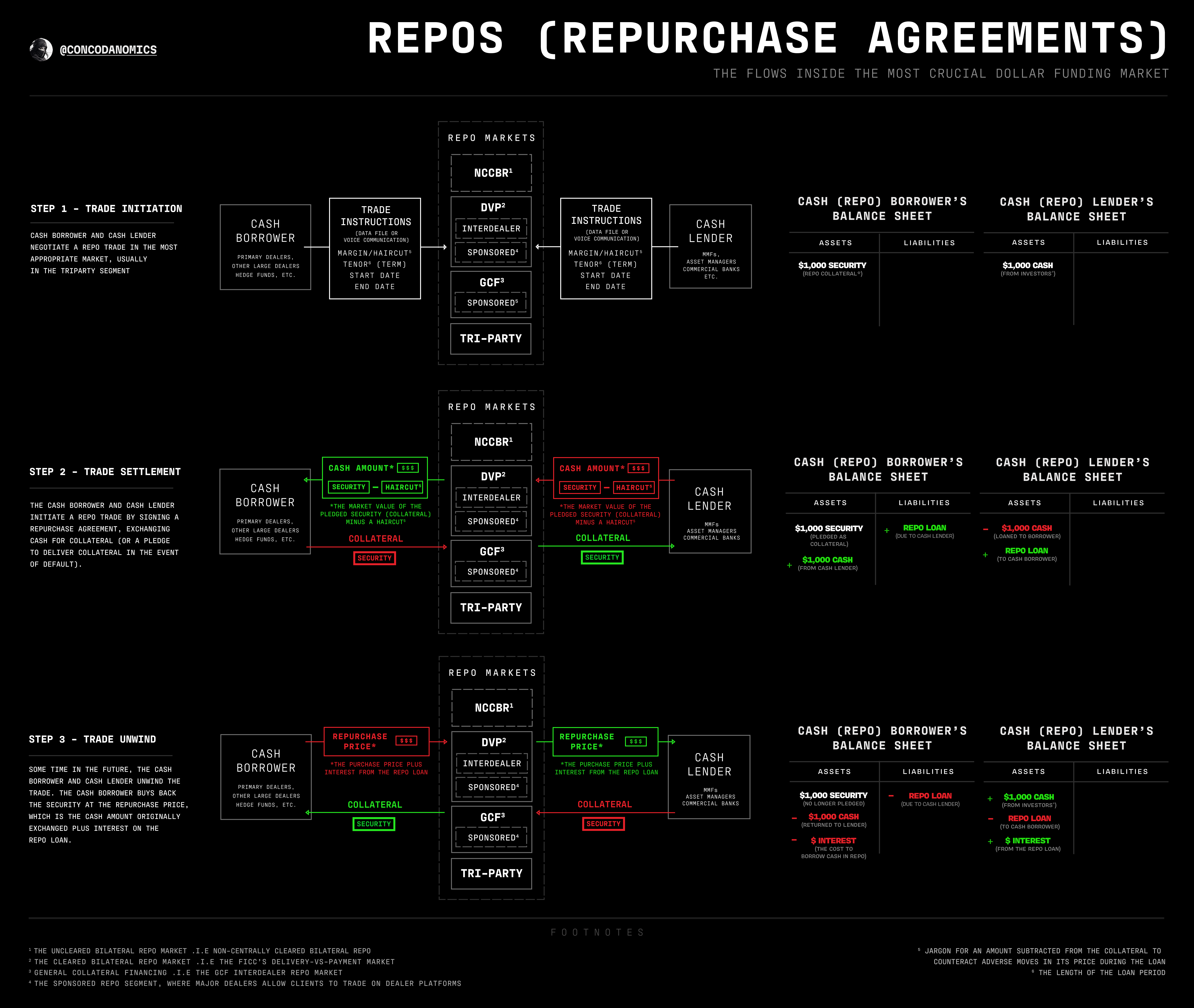

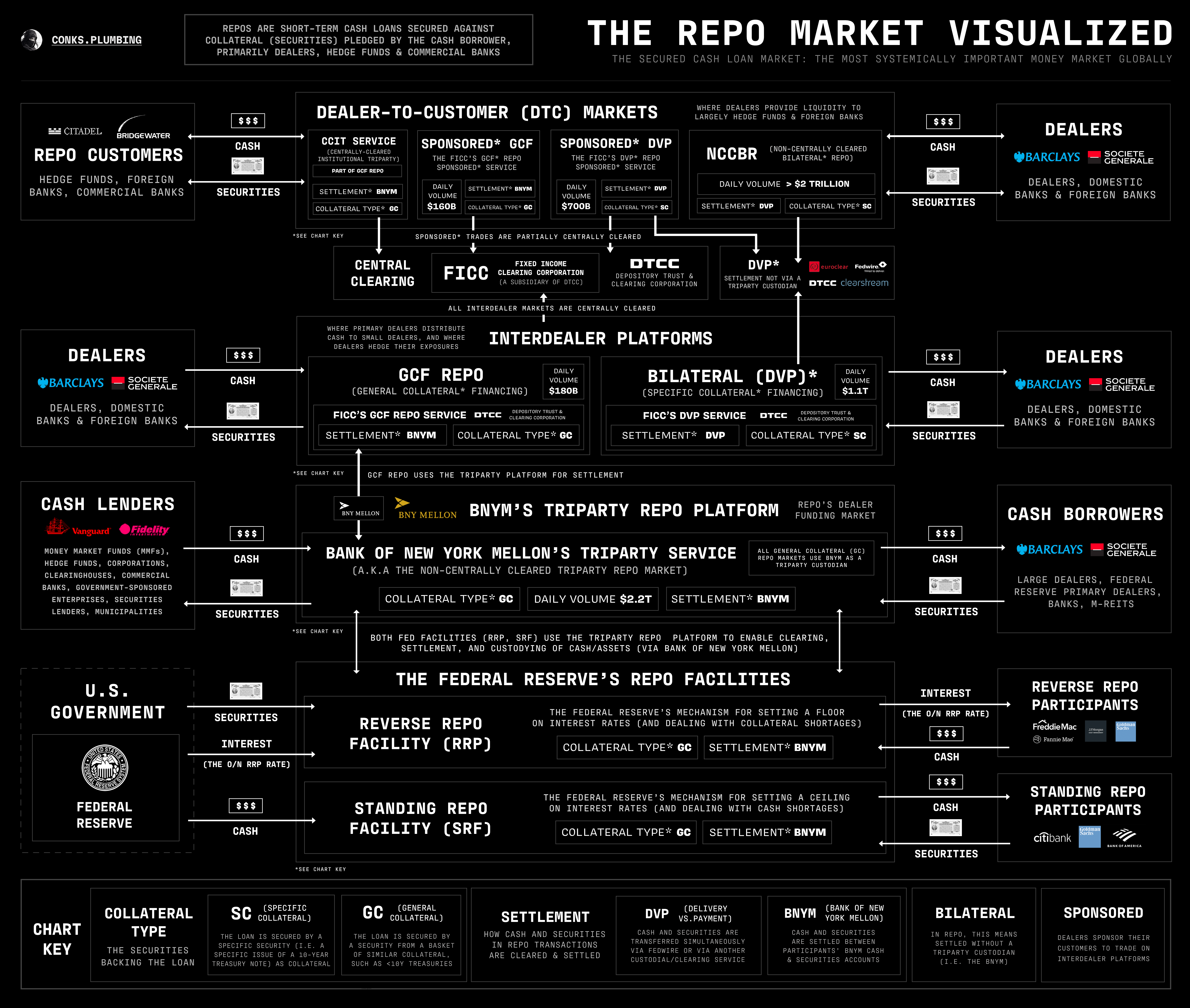

The multi-trillion-dollar repo market remains the most elaborate financial ecosystem on the planet. Unlike most regions of the global financial system, which are well observed and understood, the market for repos — short-term cash loans secured against securities as collateral — has stayed obscure. So much so that the least transparent region has grown to become the largest and most influential: the dealer-to-customer market. Here, dealers provide repos (temporary swaps of securities for cash) and reverse repos (temporary swaps of cash for securities), which they fund by borrowing cash in the triparty market, repo’s “dealer funding” market, and trading in the interdealer markets, where dealers trade repos (again, swapping cash and securities temporarily) among themselves.

{kind=link}

The end goal of repos traded outside the dealer-to-customer market is to ultimately finance repos inside the dealer-to-customer segment, the plumbing of which is specially designed for dealers to facilitate trading activities of their true “customers”: hedge funds and other speculative players — such as REITs, banks, and insurance companies — engaging in leveraged bets on (mostly government-issued) financial assets, primarily U.S. Treasuries. Somewhat unintentionally, these speculative trades create more liquid, thus more efficient sovereign debt markets, helping to power America’s financial hegemony.

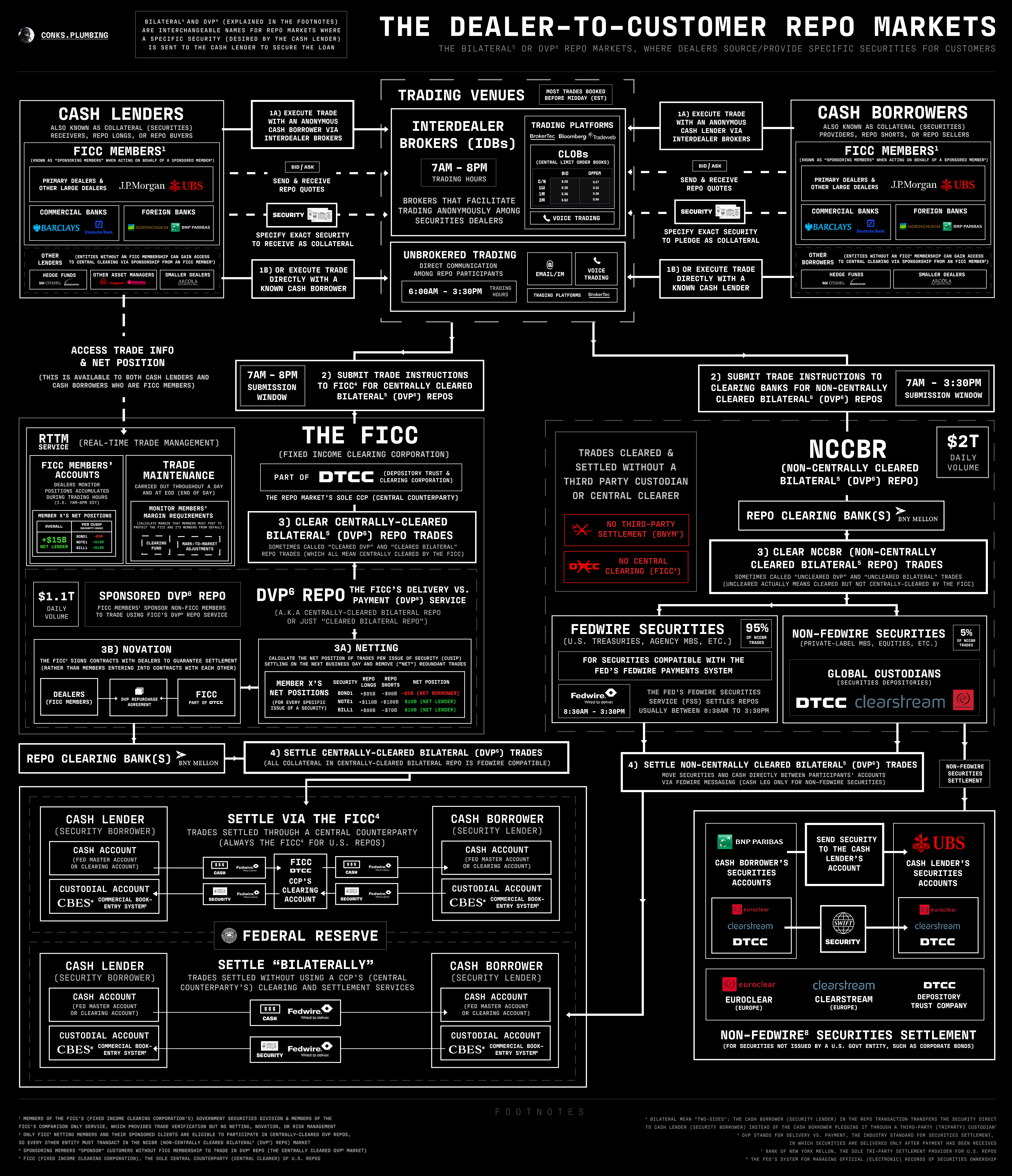

Enabling trillions in speculative trading volumes daily is the defining feature of the dealer-to-customer market: how securities pledged in repos as collateral are “settled” — i.e. transferred between participants. Dealer-to-customer repos remain the only type of repo that enables the transfer of securities between participants’ accounts during trades — unlike other repo markets that merely record the securities as pledged on relevant trading systems. These direct securities transfers allow the repo participant who’s lending cash and receiving securities as insurance to trade this “collateral” (another name for the securities received) in the secondary markets — like the Treasury cash market, before returning them (or other identical securities) to exit repo trades. Hedge funds, for instance, will enter a leveraged long position (far exceeding their available cash on hand) in a U.S. Treasury security by buying one in the secondary Treasury market and enabling this purchase by borrowing cash in a repo. It will then post the security as collateral to the dealer in the same repo used to raise cash for its initial Treasury purchase. To exit the trade, the hedge fund simply sells the Treasury security and uses the cash proceeds to repay (and thus close) the repo it used to enter its leveraged long position.

{kind=link}

Only the plumbing of the dealer-to-customer repo market, however, enables such trading. Hedge funds must obtain and deliver securities via their official securities accounts, not only to repo dealers but to buyers and sellers of U.S. Treasuries in the secondary market. For this to happen, these assets move between participants’ official securities accounts housed on Fedwire, the Federal Reserve’s system for storing and transferring official “book-entry” (jargon for electronic) records of U.S. government securities, plus securities issued by U.S. government-sponsored enterprises — such as the agency bonds of Fannie Mae & Freddie Mac.

To enable optimal settlement of U.S. government securities trades, the Federal Reserve employs a mechanism known as “DVP”, short for “delivery versus payment”. In what’s known as DVP settlement, the delivery of securities and the associated cash payment must only be settled simultaneously. When either the required funds or securities are missing from participants’ accounts, Fedwire will consequently fail to process both sides of the transaction. Thus, “delivery” occurs only “versus payment.” Because all dealer-to-customer repo trades settle via Fedwire’s DVP mechanism, the dealer-to-customer repo market is also commonly called the “DVP repo market” or “DVP repo” for short. DVP repos are thereby another term for dealer-to-customer repos, with the “customer” in “dealer-to-customer” (thus DVP repos) consisting of sophisticated players looking to speculate and engage in leveraged trading, not risk-averse cash investors such as money market funds (MMFs), which aim solely to earn interest from investing cash — using securities pledged to them in repos as insurance for their cash lending, not for deploying into elaborate trading strategies.

Despite all of its transactions settling via Fedwire’s DVP mechanism, the dealer-to-customer repo market has been split in two, divided by whether or not cash and securities also pass through the accounts of the FICC (Fixed Income Clearing Corporation), the lone central counterparty (CCP) that provides centrally cleared repo trades. Upon repo participants sending cash and securities (as margin) to its “clearing fund” — essentially a collective pot of money, the FICC guarantees settlement of cash and securities swapped in DVP repos by intervening when necessary via the Fedwire system. CCPs like the FICC will use cash accumulated in their clearing funds to offset a participant’s losses from a counterparty default, dispatching cash or securities to the affected accounts. Trades employing the FICC’s safeguards are known as centrally cleared repos — and sometimes as “cleared repos,” shortened for simplicity, not clarity, as every repo trade goes through clearing (i.e. the process of arranging settlement). For cleared repos settling via Fedwire’s DVP mechanism1, parties submit trades to the FICC’s DVP Service, in which the FICC organizes cash and securities traded in a DVP repo to be transferred via Fedwire while also guaranteeing settlement. Though the FICC’s DVP service has been classed officially as an interdealer market, it’s turned into a dealer-to-customer market, with dealers mainly intermediating cash from MMFs to hedge funds.

Meanwhile, the market for DVP repos that settle outside the FICC, i.e. directly between participants’ accounts over Fedwire, has been assigned the unfortunate name of “non-centrally cleared bilateral repo” or NCCBR. Its convoluted name derives from how trades aren’t centrally cleared by a CCP, hence “non-centrally cleared” or sometimes “uncleared” — again, shortened for simplicity, not clarity, as all repo trades are cleared in some capacity. “Bilateral” describes how NCCBR trades settle on a “bilateral basis”, jargon for how securities aren’t custodied by a third party during the repo and instead move directly between participants’ securities accounts. Whether centrally cleared or not, all DVP repos settle bilaterally. Accordingly, a “bilateral repo” is (yet another) term to describe DVP repos (thus dealer-to-customer repos). Not confusing at all.

Together with the FICC’s DVP Service, the NCCBR market forms a liquid ecosystem for dealer-to-customer repos, a repo market for leveraged speculators that tops $5 trillion in daily volumes.

To facilitate the world’s sizeable thirst for leveraged trading in U.S. government securities, dealers partake in an endless game of “repo hot potato,” swapping securities for cash via repos and cash for securities via reverse repos and charging a fee for providing liquidity. This game occurs not only in dealer-to-customer markets but in every other repo segment. In the most common chain, an MMF will lend dollars short-term to a dealer in triparty, the dealer funding market, swapping dollars for securities. The dealer will then swap dollars for securities with another dealer or a speculative customer in the other repo markets and use the collateral received to back its initial dollar borrowing — or finance another chain of repo transactions. The MMFs earn a secure return on investors’ cash, while dealers provide speculators with the ample liquidity they desire. For the Fed’s primary dealers, now providing the vast majority of repo liquidity, this game of hot potato never ends. After streamlining trillions of dollars in repos every day, primary dealers’ repo chains have grown immensely.

Yet most of these chains have also expanded in the shadows, specifically within the uncleared — thereby opaque — region of the dealer-to-customer repo market, where the most sophisticated game of repo hot potato ensues. To demystify this contest, plus uncover the intricacies of the most elaborate part of the financial system, let’s take an extensive dive into the plumbing of NCCBR: non-centrally cleared bilateral repo.